Finance Minister (FM) Nirmala Sitharaman has presented the Union Budget 2020 of India on the 1st of February, 2020. The government has taken some measures towards reaching the target of a $5 trillion economy by the end of 2022.

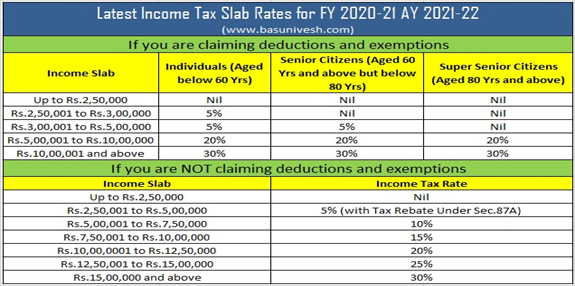

The government has proposed a new Income tax regime under Section 115BAC that comprises a significant change in the tax slabs rates. Taxpayers have been provided with an option whether they want to pay taxes according to the new regime or continue paying taxes according to the existing regime. However, a few taxpayers may not be able to switch back to the existing tax slab once they opt to follow the new one.

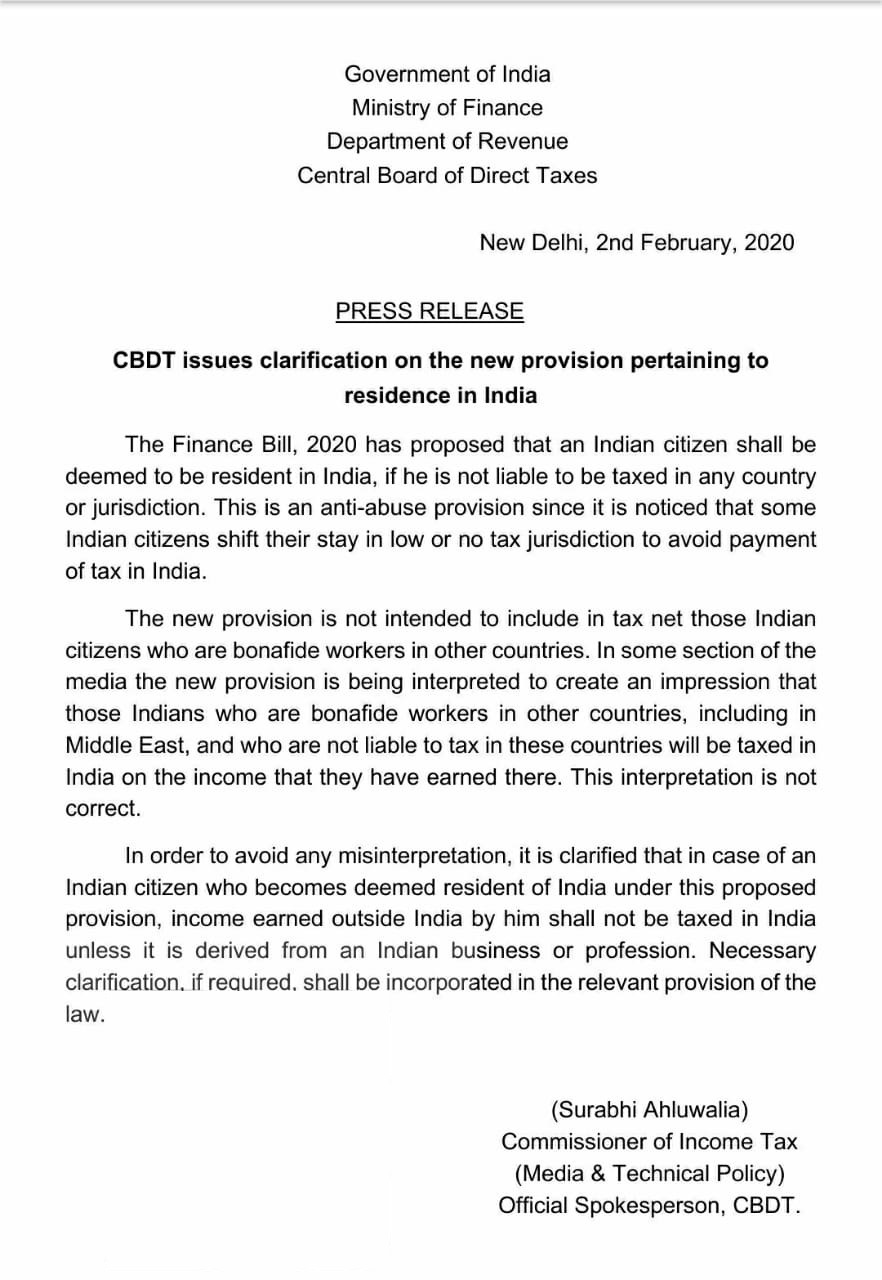

An individual is said to be resident in India in any previous year, if he— 1. is in India in that year for a period or periods amounting in all to One hundred and eighty two days or more in that year which is amended to one hundred and twenty daysor more in that year (w.e.f 1st day of April, 2021) or, 2. having within the four years preceding that year been in India for a period or periods amounting in all to three hundred and sixty-five days or more, is in India for a period or periods amounting in all to sixty days or more in that year. An individual being a citizen of India, or a person of Indian origin within the meaning of Explanation to clause (e) of section 115C*, who, being outside India, comes on a visit to India in any previous year, he will be treated as a resident in India, ? is in India for a period or periods amounting in all to one hundred and eighty two(182) days or more in that year which is amended to one hundred and twenty daysor more in that year w.e.f 1st day of April, 2021, Any individual being a citizen of India, shall be deemed to be resident in India in any previous year, if he is not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature.Please also see the clarification issued by CBDT dated 02nd February, 2020 on this matter which is given at the end of this material.

A person is said to be "not ordinarily resident" in India in any previous year if such person is—

|

Existing Provisions |

Proposed provision |

|

An individual who has been a non-resident in India in nine out of the ten previous years preceding that year, or has during the seven previous years preceding that year been in India for a period of, or periods amounting in all to, seven hundred and twenty-nine days or less; or |

An individual who has been a non-resident in India in seven out of the ten previous years preceding that year; or |

|

A Hindu undivided family whose manager has been a non-resident in India in nine out of the ten previous years preceding that year, or has during the seven previous years preceding that year been in India for a period of, or periods amounting in all to, seven hundred and twenty-nine days or less. |

A Hindu undivided family whose manager has been a non-resident in India in seven out of the ten previous years preceding that year.’ |

|

Existing Provision |

Proposed Provision |

|

The principal officer of an Indian company or a company which has made the prescribed arrangements for the declaration and payment of dividends within India, shall, before making any payment in cash or before issuing any cheque or warrant in respect of dividend, deduct from the amount of such dividend, income tax at the rates in force. |

The principal officer of an Indian company or a company which has made the prescribed arrangements for the declaration and payment of dividends within India, shall, before making any payment by any mode in respect of dividend, deduct from the amount of such dividend, income tax at 10%.

|

|

Provided that no such deduction shall be made in the case of a shareholder, being an individual, if—

(a) the dividend is paid by the company by an account payee cheque; and

(b) the amount of such dividend or, as the case may be, the aggregate of the amounts of such dividend distributed or paid or likely to be distributed or paid during the financial year by the company to the shareholder, does not exceed two thousand five hundred rupees: |

Provided that no such deduction shall be made in the case of a shareholder, being an individual, if—

(a) the dividend is paid by the company by any mode other than cash

(b) the amount of such dividend or, as the case may be, the aggregate of the amounts of such dividend distributed or paid or likely to be distributed or paid during the financial year by the company to the shareholder, does not exceed five thousand rupees: |

Section 194J stated that any person who is paying any fees to any resident person for professional or technical services rendered, then TDS is required to be deducted u/s 194 J.

Any person, not being an individual or a Hindu undivided family, who is responsible for paying to a resident any sum by way of—

i. Fees for professional services; or

ii. Fees for technical services; or

iii. Royalty; or

iv. Any remuneration or fees or commission to a director of a company other than covered u/s 192

|

Existing Provision |

Proposed provision |

|

|

Services rendered by a person in the course of carrying on any of the following professions:

» Legal profession; or

» Medical profession; or

» Engineering profession; or

» Architectural profession; or

» Profession of accountancy; or

» Profession of technical consultancy; or

» Profession of interior decoration or advertising; or

» Such other profession as notified by the Board for the purposes of Section 44AA.

Technical service means any consideration for the rendering of any managerial, technical or consultancy services but does not include consideration for any construction, assembly, and mining or like project undertaken by the recipient or consideration which would be income of the recipient chargeable under the head “Salaries.”

Any person responsible for paying to a resident any income in respect of –

a) Units of mutual fund specified under clause (23D) of section 10

b) Units from the administrator of the specified undertaking : or

c) Units from the specified company

Shall at the time of credit of such income to the account of the payee or at the time of payment thereof by any mode, whichever is earlier , deduct income tax thereon at the rate of 10%.

Provided that,

the provision of this section shall not apply where the amount of such income or, as the case may be, the aggregate of amounts of such income credited or paid by the person responsible for making the payment to the payee does not exceed Rs.5000.

Any person, being E – Commerce Operator facilitating sale of goods or provision of services of an E – Commerce participant through its electronic facility or platform is responsible to deduct TDS u/s 194O.Itis mandatory to fulfill both preconditions which are conjunctive and not dis conjunctive i.e. person must own, operate or manage Digital/Electronic Facility or Platform.

Tax should be deducted either at the time of credit of amount of sale or services, or both to the account of E – Commerce participant or at the time of payment by any mode whichever is earlier.TDS is to be deducted at 1%>on the gross amount of sales or services or both. In the Absence of Pan/Aadhaar, TDS is to be deducted @5%.It is pertinent to note that proposed section uses word “Gross amount of such Sales” which means e-commerce operator will require to deduct TDS on GST portion of sales and as well as on Commission and affiliation portion also which e-commerce operator himself will withhold.

In section 192 of the Income-tax Act the following sub-section shall be inserted (w.e.f.01.04.2021)

A person, being an eligible start-up referred to in *section 80-IAC, responsible for paying any income to the assessee being perquisite of the nature specified in clause (vi) of sub-section (2) of section 17i.e. (ESOP) in any previous year relevant to the assessment year, beginning on or after the 1st day of April, 2021, shall deduct or pay, as the case may be, tax on such income within fourteen days:-

i. After the expiry of forty-eight months from the end of the relevant assessment year, or

ii. from the date of the sale of such specified security or sweat equity share by the assessee; or

iii. From the date of the assessee ceasing to be the employee of the person

Whichever is the earliest, on the basis of rates in force for the financial year in which the said specified security or sweat equity share is allotted or transferred.”

P.T Joy | March 5, 2020

Terms of use | Privacy Policy | Contact us

© 2020 P T Joy & Associates. All Rights Reserved

Designed and Developed by Websoul Techserve